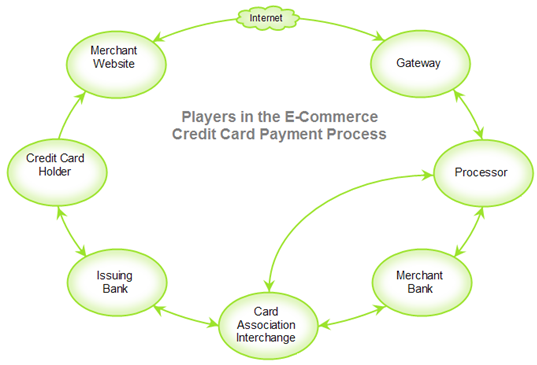

The diagram below highlights the main players in the internet e-commerce payment processing cycle.

- When a cardholder makes a purchase on a merchant website, the transaction is usually sent securely over the internet to a a Gateway such as Authorize.net or Network Merchants.

- The Gateway forwards the transaction information to a Processor (front-end processor) as part of the authorization process.

- The Processor in turn forwards the transaction information through a Card Association network such as Visa or MasterCard.

- Finally, the transaction information is routed to the Issuing Bank, which is the bank that issued the cardholder's credit or debit card in the first place. The Issuing Bank authorizes or declines the transaction.

- The authorization information is then routed back in reverse order through the Card Association back to the Processor, Gateway and finally the merchant website.

- At the end of each business day, the Gateway sends a batch of authorized transactions to the Processor for settlement.

- The list of transactions to be settled is sent to the Merchant Bank so that it can credit the merchant for the value of the transactions in the batch.

- The Merchant Bank sends individual transactions to the Card Associations. The Card Associations send a payment to the Merchant Bank for the value of the settled transactions.

- The Card Association routes the settled transactions to the appropriate Issuing Bank and drafts a payment from Issuing Bankto cover the cost of the settled transactions.

- The Issuing Bank posts the transaction to the cardholder's account. The transaction will show up on the cardholders's next monthly statement for payment.

As you might imagine, all of the actors that play a role in this process expect to be paid for the services they provide.

- Gateways typically charge monthly and per transaction fees directly to the merchant.

- Card Associations are paid an Assessment on each transaction. Assessment rates for Visa and Mastercard range from 0.11% (0.0011) to 0.13% (0.0013).

- The Issuing Bank is paid out of Interchange Fees and Dues that are paid out on each transaction.

- The Merchant Bank and Processor are paid for their role in the process (authorization, settlement, risk management, reporting, etc.).

- Discount Pricing: The most common approach is for the Merchant Bank to charge a discount rate on each transaction. The Merchant Bank keeps what is left after paying Interchange dues, fees, assessments and Processor costs.

- Interchange Plus Pricing: with Interchange Plus (or Cost Plus) pricing, a fixed mark-up is assessed on each transaction. The Merchant Bank (or Merchant Service Provider) keeps what is left of the fixed mark-up after first paying processing costs.